false0001821806P4Y02021-03-31Carries interest at a specified margin over LIBOR of 3.50% with a minimum LIBOR of 0.00%. Carries interest at a specific margin of 0.75% and 1.00% with respect to Base Rate loans and between 1.75% and 2.00% with respect to Eurodollar Rate loans with a minimum LIBOR of 0.75%. 0001821806 2020-10-04 2021-01-02 0001821806 2019-09-29 2020-10-03 0001821806 2019-09-29 2019-12-28 0001821806 2017-10-01 2018-09-29 0001821806 2018-09-30 2019-09-28 0001821806 2019-09-28 0001821806 2020-10-03 0001821806 2021-01-02 0001821806 2020-11-03 0001821806 2018-09-30 2019-10-03 0001821806 2017-09-29 2018-10-03 0001821806 2019-12-28 0001821806 2020-11-30 2020-11-30 0001821806 2020-11-30 0001821806 2020-11-03 2020-11-03 0001821806 2020-09-29 2020-10-03 0001821806 2017-09-30 0001821806 2018-09-29 0001821806 us-gaap:MoneyMarketFundsMember 2020-10-03 0001821806 lesl:SeniorUnsecuredNoteDueOnAugustSixteenTwoThousandTwentyFourMember 2020-10-03 0001821806 us-gaap:LandMember 2020-10-03 0001821806 us-gaap:BuildingMember 2020-10-03 0001821806 lesl:VehiclesMachineryAndEquipmentMember 2020-10-03 0001821806 us-gaap:LeaseholdsAndLeaseholdImprovementsMember 2020-10-03 0001821806 us-gaap:OfficeEquipmentMember 2020-10-03 0001821806 lesl:SoftwareAndConstructionInProgressMember 2020-10-03 0001821806 srt:MinimumMember 2020-10-03 0001821806 srt:MaximumMember 2020-10-03 0001821806 lesl:LeaseForCorporateHeadQuartersMember 2020-10-03 0001821806 us-gaap:CommercialRealEstateMember 2020-10-03 0001821806 lesl:IncentiveUnitsMember 2020-10-03 0001821806 lesl:IncentiveUnitGrantAgreementsMember lesl:ServiceBasedIncentiveUnitGrantsMember 2020-10-03 0001821806 lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember 2020-10-03 0001821806 lesl:MailingListsMember 2020-10-03 0001821806 lesl:ABLCreditFacilityMember 2020-10-03 0001821806 us-gaap:StandbyLettersOfCreditMember lesl:ABLCreditFacilityMember 2020-10-03 0001821806 us-gaap:WorkersCompensationInsuranceMember 2020-10-03 0001821806 lesl:EmployeeGroupMedicalPlanMember 2020-10-03 0001821806 lesl:GeneralLiabilityInsuranceProgramMember 2020-10-03 0001821806 lesl:InterestRateCapAgreementMember 2020-10-03 0001821806 us-gaap:StandbyLettersOfCreditMember 2020-10-03 0001821806 us-gaap:NoncompeteAgreementsMember 2020-10-03 0001821806 us-gaap:TrademarksAndTradeNamesMember 2020-10-03 0001821806 us-gaap:CustomerRelationshipsMember 2020-10-03 0001821806 us-gaap:ComputerSoftwareIntangibleAssetMember 2020-10-03 0001821806 us-gaap:OtherIntangibleAssetsMember 2020-10-03 0001821806 us-gaap:TrademarksAndTradeNamesMember 2020-10-03 0001821806 us-gaap:MoneyMarketFundsMember 2019-09-28 0001821806 lesl:SeniorUnsecuredNoteDueOnAugustSixteenTwoThousandTwentyFourMember 2019-09-28 0001821806 us-gaap:LandMember 2019-09-28 0001821806 us-gaap:BuildingMember 2019-09-28 0001821806 lesl:VehiclesMachineryAndEquipmentMember 2019-09-28 0001821806 us-gaap:LeaseholdsAndLeaseholdImprovementsMember 2019-09-28 0001821806 us-gaap:OfficeEquipmentMember 2019-09-28 0001821806 lesl:SoftwareAndConstructionInProgressMember 2019-09-28 0001821806 lesl:IncentiveUnitsMember 2019-09-28 0001821806 lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember 2019-09-28 0001821806 lesl:MailingListsMember 2019-09-28 0001821806 lesl:ABLCreditFacilityMember 2019-09-28 0001821806 us-gaap:WorkersCompensationInsuranceMember 2019-09-28 0001821806 lesl:GeneralLiabilityInsuranceProgramMember 2019-09-28 0001821806 lesl:EmployeeGroupMedicalPlanMember 2019-09-28 0001821806 lesl:InterestRateCapAgreementMember 2019-09-28 0001821806 us-gaap:StandbyLettersOfCreditMember 2019-09-28 0001821806 us-gaap:ComputerSoftwareIntangibleAssetMember 2019-09-28 0001821806 us-gaap:CustomerRelationshipsMember 2019-09-28 0001821806 us-gaap:NoncompeteAgreementsMember 2019-09-28 0001821806 us-gaap:TrademarksAndTradeNamesMember 2019-09-28 0001821806 us-gaap:TrademarksAndTradeNamesMember 2019-09-28 0001821806 us-gaap:OtherIntangibleAssetsMember 2019-09-28 0001821806 us-gaap:AdditionalPaidInCapitalMember 2020-10-04 2021-01-02 0001821806 us-gaap:CommonStockMember 2020-10-04 2021-01-02 0001821806 srt:MinimumMember 2020-10-04 2021-01-02 0001821806 us-gaap:EmployeeStockOptionMember 2020-10-04 2021-01-02 0001821806 us-gaap:RestrictedStockMember 2020-10-04 2021-01-02 0001821806 lesl:TermLoanMember 2020-10-04 2021-01-02 0001821806 lesl:ABLCreditFacilityMember 2020-10-04 2021-01-02 0001821806 srt:MaximumMember us-gaap:LondonInterbankOfferedRateLIBORMember lesl:SeniorUnsecuredNotesMember 2020-10-04 2021-01-02 0001821806 us-gaap:LondonInterbankOfferedRateLIBORMember srt:MinimumMember lesl:SeniorUnsecuredNotesMember 2020-10-04 2021-01-02 0001821806 us-gaap:RetainedEarningsMember 2020-10-04 2021-01-02 0001821806 lesl:InterestRateCapAgreementMember 2020-10-04 2021-01-02 0001821806 us-gaap:TrademarksAndTradeNamesMember 2020-10-04 2021-01-02 0001821806 us-gaap:NoncompeteAgreementsMember 2020-10-04 2021-01-02 0001821806 us-gaap:CustomerRelationshipsMember 2020-10-04 2021-01-02 0001821806 us-gaap:ComputerSoftwareIntangibleAssetMember 2020-10-04 2021-01-02 0001821806 us-gaap:OtherIntangibleAssetsMember 2020-10-04 2021-01-02 0001821806 lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember 2020-10-04 2021-01-02 0001821806 lesl:SeniorUnsecuredNoteDueOnAugustSixteenTwoThousandTwentyFourMember 2020-10-04 2021-01-02 0001821806 us-gaap:EurodollarMember srt:MaximumMember lesl:ABLCreditFacilityMember 2020-10-04 2021-01-02 0001821806 us-gaap:EurodollarMember srt:MinimumMember lesl:ABLCreditFacilityMember 2020-10-04 2021-01-02 0001821806 us-gaap:BaseRateMember srt:MaximumMember lesl:ABLCreditFacilityMember 2020-10-04 2021-01-02 0001821806 us-gaap:BaseRateMember srt:MinimumMember lesl:ABLCreditFacilityMember 2020-10-04 2021-01-02 0001821806 us-gaap:LondonInterbankOfferedRateLIBORMember srt:MinimumMember lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember 2020-10-04 2021-01-02 0001821806 us-gaap:LondonInterbankOfferedRateLIBORMember srt:MaximumMember lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember 2020-10-04 2021-01-02 0001821806 us-gaap:TrademarksAndTradeNamesMember 2020-10-04 2021-01-02 0001821806 lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember 2021-01-02 0001821806 us-gaap:FairValueInputsLevel2Member lesl:TermLoanDueInTwentyTwentyThreeMember 2021-01-02 0001821806 lesl:MailingListsMember 2021-01-02 0001821806 lesl:ABLCreditFacilityMember 2021-01-02 0001821806 us-gaap:StandbyLettersOfCreditMember lesl:ABLCreditFacilityMember 2021-01-02 0001821806 us-gaap:LondonInterbankOfferedRateLIBORMember lesl:InterestRateCapAgreementMember 2021-01-02 0001821806 us-gaap:WorkersCompensationInsuranceMember 2021-01-02 0001821806 lesl:GeneralLiabilityInsuranceProgramMember 2021-01-02 0001821806 lesl:EmployeeGroupMedicalPlanMember 2021-01-02 0001821806 us-gaap:LondonInterbankOfferedRateLIBORMember 2021-01-02 0001821806 lesl:InterestRateCapAgreementMember 2021-01-02 0001821806 us-gaap:StandbyLettersOfCreditMember 2021-01-02 0001821806 us-gaap:OtherIntangibleAssetsMember 2021-01-02 0001821806 us-gaap:ComputerSoftwareIntangibleAssetMember 2021-01-02 0001821806 us-gaap:CustomerRelationshipsMember 2021-01-02 0001821806 us-gaap:NoncompeteAgreementsMember 2021-01-02 0001821806 us-gaap:TrademarksAndTradeNamesMember 2021-01-02 0001821806 us-gaap:TrademarksAndTradeNamesMember 2021-01-02 0001821806 us-gaap:BuildingAndBuildingImprovementsMember srt:MinimumMember 2019-09-29 2020-10-03 0001821806 us-gaap:BuildingAndBuildingImprovementsMember srt:MaximumMember 2019-09-29 2020-10-03 0001821806 lesl:VehiclesMachineryAndEquipmentMember srt:MinimumMember 2019-09-29 2020-10-03 0001821806 lesl:VehiclesMachineryAndEquipmentMember srt:MaximumMember 2019-09-29 2020-10-03 0001821806 srt:MinimumMember us-gaap:OfficeEquipmentMember 2019-09-29 2020-10-03 0001821806 us-gaap:OfficeEquipmentMember srt:MaximumMember 2019-09-29 2020-10-03 0001821806 us-gaap:LeaseholdImprovementsMember srt:MinimumMember 2019-09-29 2020-10-03 0001821806 us-gaap:LeaseholdImprovementsMember srt:MaximumMember 2019-09-29 2020-10-03 0001821806 us-gaap:AdditionalPaidInCapitalMember 2019-09-29 2020-10-03 0001821806 us-gaap:SellingGeneralAndAdministrativeExpensesMember 2019-09-29 2020-10-03 0001821806 us-gaap:InventoryValuationReserveMember 2019-09-29 2020-10-03 0001821806 lesl:IncentiveUnitGrantAgreementsMember lesl:ServiceBasedIncentiveUnitGrantsMember us-gaap:ShareBasedCompensationAwardTrancheTwoMember 2019-09-29 2020-10-03 0001821806 lesl:IncentiveUnitGrantAgreementsMember lesl:ServiceBasedIncentiveUnitGrantsMember us-gaap:ShareBasedCompensationAwardTrancheThreeMember 2019-09-29 2020-10-03 0001821806 lesl:IncentiveUnitGrantAgreementsMember lesl:ServiceBasedIncentiveUnitGrantsMember lesl:ShareBasedCompensationAwardTrancheFourMember 2019-09-29 2020-10-03 0001821806 lesl:IncentiveUnitGrantAgreementsMember lesl:ServiceBasedIncentiveUnitGrantsMember us-gaap:ShareBasedCompensationAwardTrancheOneMember 2019-09-29 2020-10-03 0001821806 lesl:ServiceBasedIncentiveUnitGrantsMember lesl:IncentiveUnitGrantAgreementsMember 2019-09-29 2020-10-03 0001821806 lesl:IncentiveUnitGrantAgreementsMember lesl:PerformanceBasedIncentiveUnitGrantsMember 2019-09-29 2020-10-03 0001821806 us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember 2019-09-29 2020-10-03 0001821806 lesl:IncentiveUnitsMember 2019-09-29 2020-10-03 0001821806 lesl:CoronavirusAidReliefAndEconomicSecurityActMember 2019-09-29 2020-10-03 0001821806 lesl:SeniorUnsecuredNotesMember 2019-09-29 2020-10-03 0001821806 lesl:DmVenturesILlcMember lesl:LeaseForCorporateHeadQuartersMember 2019-09-29 2020-10-03 0001821806 us-gaap:OtherIntangibleAssetsMember 2019-09-29 2020-10-03 0001821806 lesl:TermLoanMember 2019-09-29 2020-10-03 0001821806 lesl:ABLCreditFacilityMember 2019-09-29 2020-10-03 0001821806 us-gaap:RetainedEarningsMember srt:RevisionOfPriorPeriodChangeInAccountingPrincipleAdjustmentMember 2019-09-29 2020-10-03 0001821806 srt:RevisionOfPriorPeriodChangeInAccountingPrincipleAdjustmentMember 2019-09-29 2020-10-03 0001821806 lesl:InterestRateCapAgreementMember 2019-09-29 2020-10-03 0001821806 us-gaap:RetainedEarningsMember 2019-09-29 2020-10-03 0001821806 lesl:SeniorUnsecuredNoteDueOnAugustSixteenTwoThousandTwentyFourMember 2019-09-29 2020-10-03 0001821806 lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember 2019-09-29 2020-10-03 0001821806 lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember srt:MinimumMember 2019-09-29 2020-10-03 0001821806 us-gaap:LondonInterbankOfferedRateLIBORMember lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember 2019-09-29 2020-10-03 0001821806 us-gaap:LondonInterbankOfferedRateLIBORMember srt:MaximumMember lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember 2019-09-29 2020-10-03 0001821806 us-gaap:LondonInterbankOfferedRateLIBORMember srt:MinimumMember lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember 2019-09-29 2020-10-03 0001821806 us-gaap:BaseRateMember srt:MinimumMember lesl:ABLCreditFacilityMember 2019-09-29 2020-10-03 0001821806 us-gaap:BaseRateMember srt:MaximumMember lesl:ABLCreditFacilityMember 2019-09-29 2020-10-03 0001821806 us-gaap:EurodollarMember srt:MinimumMember lesl:ABLCreditFacilityMember 2019-09-29 2020-10-03 0001821806 us-gaap:EurodollarMember srt:MaximumMember lesl:ABLCreditFacilityMember 2019-09-29 2020-10-03 0001821806 us-gaap:AdditionalPaidInCapitalMember 2018-09-30 2019-09-28 0001821806 us-gaap:SellingGeneralAndAdministrativeExpensesMember 2018-09-30 2019-09-28 0001821806 us-gaap:InventoryValuationReserveMember 2018-09-30 2019-09-28 0001821806 lesl:TermLoanMember lesl:AmendmentOfTermLoanMember 2018-09-30 2019-09-28 0001821806 lesl:IncentiveUnitGrantAgreementsMember lesl:ServiceBasedIncentiveUnitGrantsMember 2018-09-30 2019-09-28 0001821806 lesl:IncentiveUnitGrantAgreementsMember lesl:PerformanceBasedIncentiveUnitGrantsMember 2018-09-30 2019-09-28 0001821806 us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember 2018-09-30 2019-09-28 0001821806 lesl:IncentiveUnitsMember 2018-09-30 2019-09-28 0001821806 lesl:DmVenturesILlcMember lesl:LeaseForCorporateHeadQuartersMember 2018-09-30 2019-09-28 0001821806 us-gaap:OtherIntangibleAssetsMember 2018-09-30 2019-09-28 0001821806 us-gaap:RetainedEarningsMember 2018-09-30 2019-09-28 0001821806 lesl:InterestRateCapAgreementMember 2018-09-30 2019-09-28 0001821806 us-gaap:AdditionalPaidInCapitalMember 2017-10-01 2018-09-29 0001821806 us-gaap:SellingGeneralAndAdministrativeExpensesMember 2017-10-01 2018-09-29 0001821806 us-gaap:InventoryValuationReserveMember 2017-10-01 2018-09-29 0001821806 lesl:IncentiveUnitGrantAgreementsMember lesl:ServiceBasedIncentiveUnitGrantsMember 2017-10-01 2018-09-29 0001821806 lesl:IncentiveUnitGrantAgreementsMember lesl:PerformanceBasedIncentiveUnitGrantsMember 2017-10-01 2018-09-29 0001821806 us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember 2017-10-01 2018-09-29 0001821806 lesl:IncentiveUnitsMember 2017-10-01 2018-09-29 0001821806 us-gaap:RetainedEarningsMember 2017-10-01 2018-09-29 0001821806 lesl:DmVenturesILlcMember lesl:LeaseForCorporateHeadQuartersMember 2017-10-01 2018-09-29 0001821806 us-gaap:OtherIntangibleAssetsMember 2017-10-01 2018-09-29 0001821806 lesl:InterestRateCapAgreementMember 2017-10-01 2018-09-29 0001821806 us-gaap:AdditionalPaidInCapitalMember 2019-09-29 2019-12-28 0001821806 srt:RevisionOfPriorPeriodChangeInAccountingPrincipleAdjustmentMember 2019-09-29 2019-12-28 0001821806 us-gaap:RetainedEarningsMember srt:RevisionOfPriorPeriodChangeInAccountingPrincipleAdjustmentMember 2019-09-29 2019-12-28 0001821806 us-gaap:RetainedEarningsMember 2019-09-29 2019-12-28 0001821806 us-gaap:OtherIntangibleAssetsMember 2019-09-29 2019-12-28 0001821806 us-gaap:ComputerSoftwareIntangibleAssetMember 2019-09-29 2019-12-28 0001821806 us-gaap:TrademarksAndTradeNamesMember 2019-09-29 2019-12-28 0001821806 us-gaap:NoncompeteAgreementsMember 2019-09-29 2019-12-28 0001821806 us-gaap:CustomerRelationshipsMember 2019-09-29 2019-12-28 0001821806 us-gaap:TrademarksAndTradeNamesMember 2019-09-29 2019-12-28 0001821806 lesl:PennsylavaniaMember lesl:SwimmingPoolSpaSuppliesAndGroundPoolsMember 2018-01-01 2018-01-31 0001821806 lesl:PennsylavaniaMember us-gaap:RealEstateMember 2018-01-01 2018-01-31 0001821806 lesl:AzMember 2018-05-01 2018-05-31 0001821806 lesl:PacificNorthwestMember 2019-01-01 2019-01-31 0001821806 stpr:OR 2019-10-01 2019-10-31 0001821806 us-gaap:LondonInterbankOfferedRateLIBORMember lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember srt:MaximumMember 2018-02-27 2018-02-27 0001821806 us-gaap:LondonInterbankOfferedRateLIBORMember lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember srt:MinimumMember 2018-02-27 2018-02-27 0001821806 lesl:InterestRateCapAgreementMember 2020-09-29 2020-10-03 0001821806 us-gaap:TrademarksAndTradeNamesMember 2020-09-29 2020-10-03 0001821806 us-gaap:NoncompeteAgreementsMember 2020-09-29 2020-10-03 0001821806 us-gaap:CustomerRelationshipsMember 2020-09-29 2020-10-03 0001821806 us-gaap:ComputerSoftwareIntangibleAssetMember 2020-09-29 2020-10-03 0001821806 us-gaap:OtherIntangibleAssetsMember 2020-09-29 2020-10-03 0001821806 us-gaap:TrademarksAndTradeNamesMember 2020-09-29 2020-10-03 0001821806 lesl:SeniorUnsecuredNotesMember 2020-11-03 0001821806 lesl:IncentiveUnitsMember 2018-09-29 0001821806 lesl:InterestRateCapAgreementMember 2018-09-29 0001821806 us-gaap:SubsequentEventMember us-gaap:IPOMember 2020-11-02 2020-11-02 0001821806 us-gaap:SubsequentEventMember 2020-11-02 2020-11-02 0001821806 us-gaap:SubsequentEventMember us-gaap:IPOMember 2020-11-02 0001821806 us-gaap:EurodollarMember lesl:ABLCreditFacilityMember srt:MaximumMember 2020-08-13 2020-08-13 0001821806 us-gaap:EurodollarMember lesl:ABLCreditFacilityMember srt:MinimumMember 2020-08-13 2020-08-13 0001821806 lesl:ABLCreditFacilityMember srt:MinimumMember us-gaap:BaseRateMember 2020-08-13 2020-08-13 0001821806 lesl:ABLCreditFacilityMember srt:MaximumMember us-gaap:BaseRateMember 2020-08-13 2020-08-13 0001821806 us-gaap:LondonInterbankOfferedRateLIBORMember lesl:InterestRateCapAgreementMember 2017-03-31 0001821806 lesl:InterestRateCapAgreementMember 2017-03-31 0001821806 lesl:InterestRateCapAgreementMember 2017-03-01 2017-03-31 0001821806 lesl:ABLCreditFacilityMember 2019-12-28 0001821806 lesl:TermLoanDueOnAugustSixteenTwoThousandAndTwentyThreeMember 2019-12-28 0001821806 lesl:SeniorUnsecuredNoteDueOnAugustSixteenTwoThousandTwentyFourMember 2019-12-28 0001821806 lesl:MailingListsMember 2019-12-28 0001821806 us-gaap:CustomerRelationshipsMember 2019-12-28 0001821806 us-gaap:NoncompeteAgreementsMember 2019-12-28 0001821806 us-gaap:TrademarksAndTradeNamesMember 2019-12-28 0001821806 us-gaap:TrademarksAndTradeNamesMember 2019-12-28 0001821806 us-gaap:ComputerSoftwareIntangibleAssetMember 2019-12-28 0001821806 us-gaap:OtherIntangibleAssetsMember 2019-12-28 0001821806 us-gaap:IPOMember 2020-11-30 2020-11-30 0001821806 us-gaap:IPOMember lesl:SeniorUnsecuredNotesMember 2020-11-30 2020-11-30 0001821806 us-gaap:RetainedEarningsMember 2020-10-03 0001821806 us-gaap:AdditionalPaidInCapitalMember 2020-10-03 0001821806 us-gaap:CommonStockMember 2020-10-03 0001821806 us-gaap:RetainedEarningsMember 2021-01-02 0001821806 us-gaap:AdditionalPaidInCapitalMember 2021-01-02 0001821806 us-gaap:CommonStockMember 2021-01-02 0001821806 us-gaap:InventoryValuationReserveMember 2019-09-28 0001821806 us-gaap:InventoryValuationReserveMember 2020-10-03 0001821806 us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember 2019-09-28 0001821806 us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember 2020-10-03 0001821806 us-gaap:InventoryValuationReserveMember 2018-09-29 0001821806 us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember 2018-09-29 0001821806 us-gaap:CommonStockMember 2019-09-28 0001821806 us-gaap:AdditionalPaidInCapitalMember 2019-09-28 0001821806 us-gaap:RetainedEarningsMember 2019-09-28 0001821806 us-gaap:CommonStockMember 2017-09-30 0001821806 us-gaap:AdditionalPaidInCapitalMember 2017-09-30 0001821806 us-gaap:RetainedEarningsMember 2017-09-30 0001821806 us-gaap:InventoryValuationReserveMember 2017-09-30 0001821806 us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember 2017-09-30 0001821806 lesl:IncentiveUnitsMember 2017-09-30 0001821806 us-gaap:CommonStockMember 2018-09-29 0001821806 us-gaap:AdditionalPaidInCapitalMember 2018-09-29 0001821806 us-gaap:RetainedEarningsMember 2018-09-29 0001821806 us-gaap:RetainedEarningsMember 2019-12-28 0001821806 us-gaap:AdditionalPaidInCapitalMember 2019-12-28 0001821806 us-gaap:CommonStockMember 2019-12-28 utr:Year iso4217:USD xbrli:shares xbrli:pure lesl:Locations iso4217:USD xbrli:shares lesl:States

As filed with the Securities and Exchange Commission on February 8, 2021

SECURITIES AND EXCHANGE COMMISSION

THE SECURITIES ACT OF 1933

(Exact name of Registrant as specified in its charter)

|

|

|

|

|

|

|

|

|

|

(State or other jurisdiction of incorporation |

|

(Primary Standard Industrial Classification Code Number) |

|

(I.R.S. Employer Identification Number) |

2005 East Indian School Road

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Senior Vice President, General Counsel

2005 East Indian School Road

(Name, address, including zip code, and telephone number, including area code, of agent for service)

|

|

|

Jennifer Bellah Maguire

Peter W. Wardle Gibson, Dunn & Crutcher LLP |

|

Marc D. Jaffe

Stelios G. Saffos Latham & Watkins LLP 885 Third Avenue New York, New York 10022 (212) 906-1200 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box.

☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule

12b-2

of the Exchange Act.

|

|

|

|

|

|

|

|

|

| Large accelerated filer ☐ |

|

Accelerated filer ☐ |

|

Non-accelerated filer ☒ |

|

Smaller reporting company ☐ |

|

Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

☐

CALCULATION OF REGISTRATION FEE

|

|

|

|

|

|

|

|

|

| |

Securities to be Registered |

|

|

|

Proposed

Maximum

Aggregate

Offering Price |

|

|

|

|

| Common Stock, $0.001 par value per share |

|

33,350,000 |

|

$29.86 |

|

$995,831,000 |

|

$108,64 6 |

| |

| |

| (1) |

Includes 4,350,000 shares of common stock that the underwriters have the option to purchase. See “Underwriting.” |

| (2) |

Estimated solely for the purpose of calculating the registration fee under Rule 457(c) of the Securities Act of 1933, as amended, based on the average of the high and low prices of a share of common stock on The Nasdaq Global Select Market on February 4, 2021, which was $29.86. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. The securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Preliminary Prospectus dated February 8, 2021

The selling stockholders identified in this prospectus are offering 29,000,000 shares of our common stock. We will not receive any proceeds from the sale of shares of our common stock by the selling stockholders.

Our common stock is listed on The Nasdaq Global Select Market (“Nasdaq”) under the symbol “LESL.” On February 5, 2021, the last reported sales price of a share of our common stock on Nasdaq was $28.05.

Investing in our common stock involves risks. See the section titled “

Risk Factors,” beginning on page 16 for a discussion of information that should be considered in connection with an investment in our common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

|

|

|

|

|

|

|

|

|

| |

|

Per Share |

|

|

Total |

|

| |

|

$ |

|

|

|

$ |

|

|

Underwriting discounts and commissions(1) |

|

$ |

|

|

|

$ |

|

|

Proceeds to the selling stockholders, before expenses |

|

$ |

|

|

|

$ |

|

|

| (1) |

See the section titled “Underwriting” for a description of compensation payable to the underwriters and estimated offering expenses. |

The underwriters may also exercise their option to purchase up to an additional 4,350,000 shares from the selling stockholders at the public offering price less the underwriting discount for 30 days after the date of this prospectus.

The shares will be ready for delivery on or about , 2021.

The date of this prospectus is , 2021.

|

|

|

|

|

| |

|

|

|

| |

|

|

1 |

|

| |

|

|

13 |

|

| |

|

|

14 |

|

| |

|

|

16 |

|

| |

|

|

37 |

|

| |

|

|

39 |

|

| |

|

|

40 |

|

| |

|

|

41 |

|

| |

|

|

42 |

|

| |

|

|

44 |

|

| |

|

|

65 |

|

| |

|

|

83 |

|

| |

|

|

93 |

|

| |

|

|

103 |

|

| |

|

|

105 |

|

| |

|

|

110 |

|

| |

|

|

112 |

|

| |

|

|

115 |

|

| |

|

|

120 |

|

| |

|

|

128 |

|

| |

|

|

129 |

|

| |

|

|

130 |

|

| |

|

|

F-1 |

|

You should rely only on the information contained in this prospectus or in any related free-writing prospectus prepared by or on behalf of us. We, the selling stockholders and the underwriters have not authorized anyone to provide you with information different from, or in addition to, the information contained in this prospectus or in any related free-writing prospectus. The information contained in this prospectus is current only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of the shares of common stock.

We, the selling stockholders and the underwriters have not taken any action that would permit a public offering of the shares of common stock outside the United States or permit the possession or distribution of this prospectus or any related free-writing prospectus outside the United States. Persons outside the United States who come into possession of this prospectus or any related free-writing prospectus must inform themselves about and observe any restrictions relating to the offering of the shares of common stock and the distribution of the prospectus outside the United States.

Leslie’s

®

, AccuBlue

®

, MyLife

®

, and other trademarks, trade names or service marks of Leslie’s, Inc. appearing in this prospectus are the property of Leslie’s, Inc. All other trademarks, trade names, and service marks appearing in this prospectus are the property of their respective owners. Solely for convenience, the trademarks and trade names in this prospectus may be referred to without the

®

and

™

symbols, but those references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights, or the rights of the applicable licensor to these trademarks and tradenames.

Market, Ranking, and Other Industry Data

In this prospectus, we refer to information regarding industry, market, and competitive position data that we obtained from our own internal estimates and research, as well as from independent market research, industry and general publications and surveys, governmental agencies, and publicly available information in addition to research, surveys, and studies conducted by third parties. In some cases, we do not expressly refer to the sources from which this data is derived. In that regard, when we refer to one or more sources of this type of data in any paragraph, you should assume that other data of this type appearing in the same paragraph is derived from the same sources, unless otherwise expressly stated or the context otherwise requires. All of the market and industry data used in this prospectus involve a number of assumptions and limitations, and you are cautioned not to give undue weight to such assumptions and limitations.

In addition, while we believe the industry, market, and competitive position data included in this prospectus is reliable and based on reasonable assumptions, such data involve risks and uncertainties and are subject to change based on various factors, including those described in the section titled “Risk Factors.” These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties or by us.

Non-GAAP

Financial Measures

Comparable sales, comparable sales growth, adjusted EBITDA, adjusted net income and adjusted net income per share are our key

non-GAAP

financial measures. For more information about how we use these

non-GAAP

financial measures in our business, the limitations of these measures, and a reconciliation of these measures to the most directly comparable GAAP measures, please see the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations––Key Factors and Measures We Use to Evaluate Our Business.”

This summary highlights selected information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider before deciding to purchase our common stock in this offering. You should read the entire prospectus carefully, including the sections titled “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our consolidated financial statements and the related notes included elsewhere in this prospectus, before making an investment decision. If you invest in our common stock, you are assuming a high degree of risk.

Unless otherwise indicated or the context otherwise requires, all references in this prospectus to “we,” “our,” “us,” “Leslie’s,” “the Company,” and “our Company” refer to Leslie’s, Inc. and its consolidated subsidiaries.

We are committed to continuing our legacy as the most trusted authority in pool and spa care. Through our consumer-centric approach, we provide an unparalleled experience for all consumers across all channels, supported by leading product innovation, expert knowledge, and exceptional service.

We are the largest and most trusted

brand in the nearly $11 billion United States pool and spa care industry, serving residential, professional, and commercial consumers. Founded in 1963, we are the only

pool and spa care brand with national scale, operating an integrated marketing and distribution ecosystem powered by a physical network of 936 branded locations and a robust digital platform. We command a market-leading share of nearly 15% of residential aftermarket product spend as of 2019, which represents an increase of approximately 500 basis points since 2010, our physical network is larger than the sum of our twenty largest competitors, and our digital sales are estimated to be greater than five times as large as that of our largest digital competitor. We offer an extensive assortment of professional-grade products, the majority of which are exclusive to Leslie’s, as well as certified installation and repair services, all of which are essential to the ongoing maintenance of pools and spas. Our dedicated team of associates, pool and spa care experts, and experienced service technicians are passionate about empowering our consumers with the knowledge, products, and solutions necessary to confidently maintain and enjoy their pools and spas. Over the last five years, we have spent more than $70 million in foundational investments across new technologies and capabilities focused on transforming our consumer experience and advancing our industry leadership. The unprecedented scale of our integrated marketing and distribution ecosystem, which is powered by our

network, uniquely enables us to efficiently reach and service every pool and spa in the continental United States—capabilities no competitor can match.

The aftermarket pool and spa care industry is one of the most fundamentally attractive consumer categories given its scale, predictability, and growth outlook. Since 1970, when industry market data was first collected, the market has demonstrated consistent growth due to the

non-discretionary

nature of ongoing water treatment to maintain safe, sanitized water. Without proper ongoing maintenance, water quality quickly degrades, yielding unsafe conditions and risking equipment failure. As a result, each pool and spa represents an annuity-like stream of chemical, equipment, and service revenue for their average life span of over 25 years. We estimate the average

in-ground

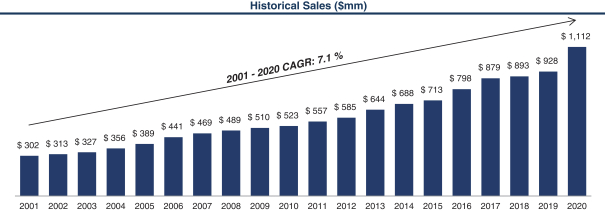

pool owner spends $24,000 or more on maintenance products and services over the life of a pool. According to P.K. Data, the United States market is comprised of a growing installed base of more than 14 million pools and spas, and the installed base of residential in ground pools has grown every year for at least 50 years. The industry generated revenue of nearly $11 billion in 2019 and grew at a 3.8% CAGR from 2015 to 2019.

The industry is currently experiencing a significant increase in demand, as the

COVID-19

pandemic has accelerated secular trends in consumer behavior. Consumers are increasingly focused on outdoor living, healthy lifestyles, sanitization and safety, migrating to lower density communities, and spending more time at home, all of which are fundamentally changing their spending patterns. In particular, the

reality of the pandemic has led to significant growth in new pool installations and pool usage. Based on research performed by P.K. Data, new pool permit activity through July 2020 has grown by 32% over the comparable period in 2019 and is forecasted to achieve unprecedented year-over-year growth in new pool installations in 2020. This significant increase in new pool construction activity represents a permanent increase in demand for aftermarket products and services. Nearly 200,000 new in ground pools are expected to be constructed in 2020 and 2021, representing nearly $5 billion in estimated lifetime maintenance spend. While our business is not dependent on new pool construction, we believe we are uniquely positioned to capture a meaningful portion of the related aftermarket spend.

Given we play primarily in the aftermarket business, we have a highly predictable, recurring revenue model, as evidenced by our 57 consecutive years of sales growth. More than 80% of our

assortment is comprised of

non-discretionary

products essential to the care of residential and commercial pools and spas. Our assortment includes chemicals, equipment and parts, cleaning and maintenance equipment, and safety, recreational, and fitness-related products. We also offer important, essential services, such as equipment installation and repair for residential and commercial consumers. Consumers receive the benefit of extended vendor warranties when purchasing product through our locations or when our certified

in-field

technicians install or repair equipment

on-site.

We also offer complimentary, commercial-grade,

in-store

water testing and analysis via our proprietary AccuBlue

®

system, which increases consumer engagement, conversion, basket size, and loyalty, resulting in higher lifetime value. Our water treatment expertise is powered by data and intelligence accumulated from the millions of water tests we have performed over our history, positioning us as the most trusted water treatment solutions provider in the industry. Due to the

non-discretionary

nature of our products and services, our business has historically delivered strong, uninterrupted growth and profitability in all market environments, including the Great Recession and the

COVID-19

pandemic. Our growth has recently accelerated, and for fiscal year 2020, our sales increased 19.8%.

57 Years of Leadership and Disruptive Innovation in Pool & Spa Care

Since our founding in 1963, we have been the leading innovator in our category and have provided our consumers with the most advanced pool and spa care available. As we have scaled, we have leveraged our competitive advantages to strategically reinvest in our business and intellectual property to develop new, value-added capabilities that allow us to meet the needs of any pool and spa owner, whether they care for their pool or spa themselves or rely on a professional, whatever the nature of their need may be, and however they wish to engage with us.

Over our

57-year

history, we have introduced innovative ways to serve pool and spa owners and the professionals who care for their pools and spas.

Owned and Exclusive Brands.

Since our inception in 1963, we have offered a portfolio of owned and exclusive brands. We continue to expand our selection of exclusive offerings through innovation, most recently with the launch of the Jacuzzi

®

and our RightFit

®

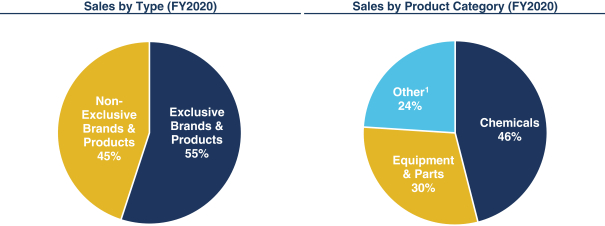

brands in 2016. Our exclusive brands and products account for approximately 55% of total sales and 80% of chemical sales. These proprietary brands and custom-formulated products are only available through our integrated platform and offer professional-grade quality to our consumers, while allowing us to achieve higher gross margins relative to sales of third-party products.

Complimentary and Proprietary Water Testing.

We pioneered complimentary

in-store

water testing, and over the course of our history have conducted millions of tests, which has helped us establish relationships, cultivate loyalty, and drive attractive lifetime value with our consumers as they rely on us for their water treatment needs. We have found that consumers who regularly test their water with us spend more with us per year than other consumers, and we believe that these consumers experience significantly fewer days where their pools are out of commission.

Complimentary

In-Store

Repair.

We provide complimentary

in-store

equipment repair, which we offer to all consumers with the purchase of Leslie’s replacement parts. Over the last fifteen years, we have conducted more than one million

in-store

repairs.

We employ the industry’s largest

in-field

service network, consisting of more than 200 pool and spa care service professionals who have the expertise to provide essential,

on-site

equipment installation and repair services for residential and commercial consumers throughout the continental United States.

In 2014, we launched the industry’s first loyalty program, which helps track loyalty members’ water treatment history and prescriptions and rewards them for shopping with us. As of October 3, 2020, our loyalty program has more than 3.3 million members, up more than 50% from 2.1 million active members as of September 2018. Our loyalty members spend twice as much with us on average compared to our other consumers.

In 2015, we made the strategic decision to resource this channel and accelerate sales growth to professional consumers. Through acquisitions, technology investments, and increased utilization of our integrated network we drove a sales CAGR of over 20% through fiscal year 2020. Our differentiated

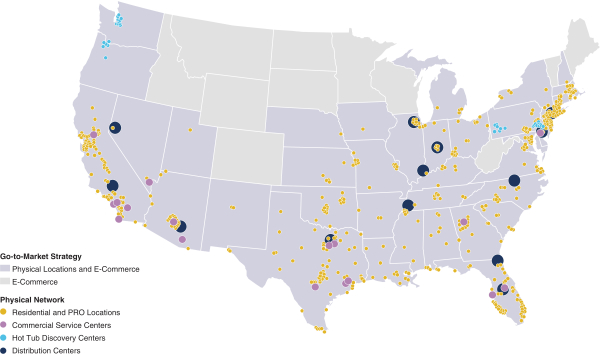

model includes 936 convenient locations, including dedicated Leslie’s PRO locations in certain markets, extended operating hours, expansive product offering through our online platforms, multiple fulfillment capabilities, and the ability to provide pool professionals with referrals to residential consumers. Despite our strong growth, our penetration in the professional market remains modest with an estimated market share of less than 10%.

Leslie’s Evolution in the Digital World

Over the last five years, we have spent more than $70 million investing in new service offerings and digital capabilities that have modernized how consumers take care of their pools and spas.

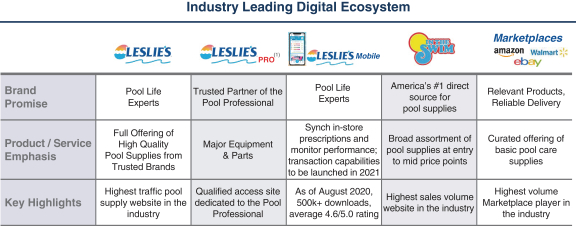

We have built the largest digital presence in the industry. Our complementary platform of branded proprietary

e-commerce

websites and marketplace storefronts allows us to seamlessly serve the needs of all digital consumers through curated pricing and targeted merchandising strategies. In addition to our owned

e-commerce

websites, approximately 40% of our digital sales take place through online marketplaces. In all, our digital network is strategically designed to maximize total profitability. Our digital sales have grown at a CAGR of more than 35% between fiscal year 2015 and fiscal year 2020, and represented 26% of our total sales in fiscal year 2020, up from 8% in fiscal year 2015.

. In 2018, we introduced a custom-designed mobile app that allows consumers to create a personalized pool profile, sync

in-store

prescriptions, and monitor the performance of

at-home

water tests. As of January 2021, the mobile app had more than one half million downloads and an average user rating of 4.6/5.0. We plan to continue enhancing this critical element of our network by introducing new features, including transaction capabilities.

Consumer-Centric Integrated Ecosystem.

We architected a consumer-centric integrated ecosystem comprised of our physical network of 936 branded locations and a robust, data-driven digital platform. Over the last two years, we have invested in new capabilities, including global inventory visibility, buy online

pick-up

in store (“BOPIS”), buy online return in store (“BORIS”), and ship from store (“SFS”), each of which will come online in 2021. With our integrated physical and digital network, we will have the unique advantage of being able to reach all consumers in the continental United States in less than 24 hours, whether they are homeowners, pool and spa professionals, or commercial pool operators, whenever, wherever, and however they prefer to shop.

In January 2020, we launched our AccuBlue

®

in-store

water testing device and enhanced water testing experience. AccuBlue

®

,

which features exclusive and proprietary software that incorporates our 57 years of accumulated water treatment expertise, automates and gamifies the water testing experience, driving enhanced accuracy, higher throughput, greater consumer engagement, and increased consumer adherence to prescription recommendations. Locations that have been equipped with AccuBlue

®

are growing sales at a faster rate than our other locations, supported by an increase in number of water tests performed, an improved conversion rate, and an increase in number of products prescribed per test which has resulted in greater units per transaction. In December 2020, we completed the rollout of AccuBlue

®

across our physical network.

Highly Experienced and Visionary Management Team.

Over the last five years, we have built a diverse, multi-disciplinary management team to drive our consumer-first, digitally enabled growth. Since 2018, four of our eight senior leaders have joined our organization, bringing new expertise and capabilities that are highly complementary and synergistic with our core industry expertise that we have accumulated over decades.

Innovating the Future of Pool and Spa Care

As we look forward, we are committed to better serving our digital-first consumer by introducing an expanded portfolio of connected pool and spa products and services. We believe that we are uniquely positioned to leverage our market-leadership to continue to disrupt the pool and spa care category and further distance ourselves from our competition.

We are actively developing new technologies that seek to fundamentally change the way all consumers, whether a novice or an expert, care for their pools and spas. Through a new AccuBlue Home

TM

subscription offering, we will leverage our proprietary water diagnostics software to convert

on-demand

test results into actionable prescriptions and treatment plans tailored to the specific size and conditions of a consumer’s pool or spa, which we can seamlessly and automatically fulfill through our integrated network.

Certified Pool Maintenance Offering.

We are assembling a strategic network of qualified pool professionals to extend the Leslie’s brand into

on-site

water maintenance, completing our suite of service offerings in the residential pool ecosystem.

We continue to leverage our intellectual property and differentiated strategic position to be the innovator and disruptor in our industry. We plan to strategically reinvest in our business and bring to market new products and services that will continue to improve our ability to serve our consumers and win in the marketplace. In addition to our internal efforts, as the most recognized and trusted authority in the industry with the most direct access and deepest relationships with pool and spa owners, we continue to receive unsolicited opportunities from third parties to introduce to the market and commercialize new products and services on an exclusive basis.

Our Competitive Strengths

We believe that the following competitive strengths have been key drivers of our success to date, and strategically position us for continued success.

Undisputed

market leader in the aftermarket pool and spa care industry.

For 57 years, we have been dedicated to addressing our consumers’ pool needs so they can spend less time maintaining and more time enjoying their pools. We are the only

pool and spa care brand with a nationwide physical presence and an integrated digital platform, consisting of individually merchandised

e-commerce

websites, a mobile app with transaction capabilities, and online marketplace operations, is designed to address the needs of all pool and spa consumers. The remainder of the industry is highly fragmented across both offline and online providers. We command a market-leading share of nearly 15% of residential aftermarket product spend, which represents an increase of approximately 500 basis points since 2010, our physical network is larger than the sum of the next twenty largest competitors, and our digital sales are estimated to be greater than five times as large as that of our largest digital competitor.

We believe that our history, scale, and consumer-centric approach have contributed to industry-leading consumer affinity metrics. As a result of our consumer-centric approach, we have a Voice of Customer (VoC) score of approximately 75% based on our regular surveys of our consumer file, which demonstrates our consumers’ strong affinity for our brand.

Direct relationships with more than 11 million pool and spa owners and professionals, generating durable, annuity-like economics.

We are the largest national pool and spa care brand that has a direct relationship with pool and spa owners and the professionals who serve them. Across our integrated platform, we have a total file of approximately 11 million consumers. Through our team of highly trained pool and spa experts, we offer sophisticated product recommendations and other expert advice, which cultivates long-standing relationships with our consumers. The comprehensive nature of our product and service offering eliminates the need for consumers to leave the Leslie’s ecosystem, driving exceptional retention with annuity-like economics.

In 2014, we launched our loyalty membership program to further deepen our consumer relationships. The program, which serves more than 3.3 million consumers, allows members to save, earn, and redeem via discounts, points, and rewards. We track consumer preferences, order frequency, and pool profiles in order to curate and enhance our recommendations and promotions, anticipate product demand, and track lifetime value to better incentivize our loyalty members. On average, a loyalty member spends twice as much with us per year than a

non-loyalty

member.

Consumer-centric connected ecosystem for all pool and spa owners and the professionals who serve them using proprietary, leading brands across all channels.

We have built the most extensive and geographically diverse pool and spa care network in the United States, consisting of three formats: Residential, Professional (PRO), and Commercial. Our locations are strategically located in densely populated areas mainly throughout the Sunbelt, including California, Arizona, Texas, and Florida. Across our physical network, we employ a team of associates, including pool and spa care experts and service technicians, who act as solution providers to all of our consumers, including both

(“DIY”) and

(“DIFM”) pool owners as well as pool professionals.

As the world has become more digitally focused, and consumers increasingly demand “smart” home-enabled options, we have focused on architecting the industry-leading integrated digital platform of proprietary

e-commerce

websites designed to serve our residential, professional, and commercial consumers. Our proprietary

e-commerce

websites serve digital consumers through curated pricing and targeted merchandising strategies. In addition to our owned

e-commerce

websites, we offer our products through online marketplaces such as Amazon, eBay, and Walmart. As a result of our strategic investments in digital, we are uniquely positioned to serve our consumers with cross-channel capabilities and capture incremental online demand from new consumers while growing the total profitability of the network.

Comprehensive assortment of proprietary brands with recurring, essential, superior product formulations, and trusted, solution-based services for all consumers.

We offer a comprehensive product assortment, consisting of more than 30,000 products across chemicals, equipment and parts, cleaning and maintenance equipment, and safety, recreational, and fitness-related categories. More than 80% of our product sales are

non-discretionary

and recurring in nature; these products are critical to the ongoing maintenance of pools and spas. In addition, approximately 55% of our total sales and 80% of our chemical sales are derived from proprietary brands and custom-formulated products, which allows us to create an entrenched consumer relationship, control our supply chain, and capture attractive margins. Consumers choose our exclusive, proprietary brands and custom-formulated products for their efficacy and value, a combination that we believe cannot be found elsewhere.

We pair our comprehensive product assortment with differentiated

in-store

and

on-site

service offerings. We pioneered the complimentary

in-store

water test and resulting pool or spa water prescription, which has driven consumer traffic and loyalty, and has created a “pharmacist-like” relationship with our consumers. Through innovation, we recently introduced significant upgrades to our water testing capabilities with the launch of our AccuBlue

®

platform. The AccuBlue

®

testing device screens for nine distinct water quality criteria. Our

in-store

experts leverage our proprietary AccuBlue

®

water diagnostics software engine to offer our consumers a customized prescription and treatment plan using our comprehensive range of exclusive products, walking them through product use sequencing

These detailed and sophisticated treatment algorithms are supported by our differentiated water treatment expertise built over decades. Historically, we have found that consumers who test their water with us regularly spend more with us per year than those who do not, underscoring the importance of this acquisition and retention vehicle. We also employ the industry’s largest network of

in-field

technicians who perform

on-site

evaluations, installation, and repair services for residential and commercial consumers.

Attractive financial profile characterized by consistent, profitable growth, and strong cash flow conversion offering multiple levers to drive shareholder value.

We have delivered 57 consecutive years of sales growth, demonstrating our ability to deliver strong financial results through all economic cycles. Our growth has been broad based across residential pool, residential spa, professional pool, and commercial pool consumers and has been driven by strong retention and profitable acquisition of sticky, long-term consumer relationships. Due to our scale, vertical integration, and operational excellence, we maintain high profitability. Due to our low maintenance capital intensity, we generate strong cash flows. As a result of our attractive financial profile, we have significant flexibility with respect to capital allocation, giving us the ability to drive long-term shareholder value through various operating and financial strategies.

Highly experienced and visionary management team that combines deep industry expertise and advanced,

capabilities.

Our strategic vision and culture are directed by our executive management team under the leadership of our Chief Executive Officer, Michael R. Egeck and our Executive Vice President and Chief Financial Officer, Steven M. Weddell. Our well-balanced executive management team is comprised of leaders with decades of experience in the pool and spa care industry as well as recently hired executives who bring new expertise and capabilities to Leslie’s from outside industries. Our management team is uniquely capable of executing upon our strategic vision and successfully continuing to create long-term shareholder value.

We believe we have significant opportunity to acquire new residential consumers and reactivate lapsed residential consumers, which we plan to do by executing on the following strategies:

| |

• |

|

Acquire or reactivate consumers via optimized marketing strategy. We believe we have a sizeable opportunity to grow by serving the millions of pool and spa owners in our market who do not actively shop with us today. We plan to accelerate our acquisition of these potential new or reactivated consumers and, at the same time, reduce consumer acquisition cost by shifting our marketing mix toward more efficient digital and social channels. |

| |

• |

|

Capture outsized share of new pool and spa consumers. We have observed considerable recent acceleration in new pool and hot tub installations, bringing new consumers to our market. We intend to bolster consumer file growth by deploying targeted marketing tactics to win outsized share of this new consumer cohort. |

Increase share of wallet among existing consumers.

We currently serve a file of approximately 5.5 million active consumers, which represents approximately

one-third

of the estimated total addressable market of pool and spa owners. We define “active consumers” as consumers who transacted with us during the 18-month period ended October 3, 2020 and “lapsed residential consumers” as those who have shopped with us in the past, but have not transacted with us in the last 18 months. We believe we have a significant opportunity to increase spend from existing consumers and drive higher lifetime value. We plan to do this by executing on the following strategies:

| |

• |

|

Increase loyalty membership penetration and introduce program upgrades. We plan to continue to market our loyalty program in-store and online to convert more of our consumers to loyalty members. In addition, we are in the process of enhancing our loyalty program to offer more value-added features and further drive member engagement. We will explore opportunities to drive interest by selectively offering special incentives and rewards as well as introducing new value-added features. We believe these initiatives will drive higher transaction frequency and basket size, which will result in increased category spend and higher lifetime value with existing consumers. |

| |

• |

|

Enhance retention marketing. While we have historically been satisfied with our consumer retention metrics, we believe there is opportunity to drive even greater retention. We plan to do this by more actively leveraging our consumer database to personalize the consumer experience with targeted messaging and product recommendations. |

| |

• |

|

Expand our product and service offering. We plan to expand our offering by introducing new and innovative products and services in our existing categories and by expanding into adjacent categories. Specifically, we believe there is an opportunity with products targeted to spa owners, who have historically been underserved. |

Grow additional share in the professional market.

We believe we have a significant opportunity to grow our sales with pool care professionals, who individually spend more than 25x as much as residential consumers on pool supplies and equipment.

Our research suggests that small and

mid-size

pool professionals value convenience and referrals, both of which we are uniquely positioned to offer given our 900+ locations and industry’s largest consumer file. We plan to expand our physical network of PRO locations, which specifically cater to pool professionals, by opening new locations and selectively remodeling existing residential locations. We believe there is significant whitespace opportunity to operate more than 200 total PRO locations across the United States. We also plan to assemble an affiliated network of qualified pool professionals to extend the Leslie’s name into water maintenance. We believe that this initiative represents a natural adjacency and will resonate with existing residential consumers as well as help attract new residential consumers.

Utilize strategic M&A to consolidate share and further enhance capabilities.

The aftermarket pool and spa industry remains highly fragmented, which offers attractive opportunities to utilize strategic M&A to drive consolidation. We have historically used, and plan to continue to use, strategic acquisitions to obtain consumers and capabilities in both new and existing markets. We believe that we are the consolidator of choice in the industry, and we will continue to focus on acquiring high quality, market-leading businesses with teams, capabilities, and technologies that uniquely position us to create value by applying best practices across our entire physical and digital network to better serve new and existing consumer types.

Addressing underserved residential whitespace.

We have identified more than 700 underserved residential pool and spa care markets in the continental United States. With our omni-channel capabilities, successful track record of new location openings, and targeted digital marketing tactics, we believe we are well positioned to capitalize on this meaningful whitespace opportunity. We plan to assess each market independently and determine the most capital efficient way to serve these trade areas using a mix of digital assets and physical locations.

Continue to introduce disruptive innovation.

Leslie’s has a legacy of disruptive innovation in the pool and spa care industry. We plan to continue that legacy by continuously developing and introducing capabilities that create value for our consumers. Present areas of focus include water testing, maintenance prescriptions, new product offerings, and our product distribution ecosystem.

As the Internet of Things wave continues, we believe consumers will seek the convenience of “smart” home functionality in more facets of their daily lives. We believe this presents an opportunity to introduce a full service, connected home solution that effectively automates pool maintenance, including actively monitoring our customer’s water, diagnosing, developing, and prescribing a treatment plan, and delivering to our customer’s home the assortment of products needed to maintain a clear, safe, beautiful pool.

Our business is subject to numerous risks described in the section entitled “Risk Factors” and elsewhere in this prospectus. You should carefully consider these risks before making an investment. Some of these risks include:

Risks Related to the Nature of Our Business

:

| |

• |

|

If we are unable to achieve comparable sales growth, our profitability and performance could be materially adversely impacted. |

| |

• |

|

Past growth may not be indicative of future growth. |

| |

• |

|

Loss of key members of management could adversely affect our business. |

| |

• |

|

We are subject to legal or other proceedings that could have a material adverse effect on us. |

| |

• |

|

Disruptions from disasters and similar events could have a material adverse effect on our business. |

Risks Related to Our Industry and the Broader Economy

| |

• |

|

We face competition by manufacturers, retailers, distributors, and service providers in the residential, professional, and commercial pool and spa care market. |

| |

• |

|

The demand for our swimming pool and spa related products and services may be adversely affected by unfavorable economic conditions. |

| |

• |

|

The outbreak of COVID-19 could adversely impact our business and results of operations. |

| |

• |

|

The demand for pool chemicals may be affected by consumer attitudes towards products for environmental or safety reasons. |

| |

• |

|

Our results of operations may fluctuate from quarter to quarter for many reasons, including seasonality. |

| |

• |

|

We are susceptible to adverse weather conditions. |

Technology and Privacy Related Risks

| |

• |

|

If our online systems do not function effectively, our operating results could be adversely affected. |

| |

• |

|

Any limitation or restriction to sell on online platforms could harm our profitability. |

| |

• |

|

A significant disturbance or breach of our technological infrastructure could adversely affect our financial condition and results of operations. |

| |

• |

|

Improper activities by third parties and other events or developments may result in future intrusions into or compromise of our networks, payment card terminals or other payment systems. |

Risks Related to Our Business Strategy

| |

• |

|

We may acquire other companies or technologies, which could fail to result in a commercial product and otherwise disrupt our business. |

| |

• |

|

Our operating results will be harmed if we are unable to effectively manage and sustain our future growth or scale our operations. |

Risks Related to the Manufacturing, Processing, and Supply of Our Products

| |

• |

|

Our business includes the packaging and storage of chemicals and an accident related to these chemicals could subject us to liability and increased costs. |

| |

• |

|

Product supply disruptions may have an adverse effect on our profitability and operating results. |

| |

• |

|

The cost of raw materials could increase our cost of goods sold and cause our results of operations and financial condition to suffer. |

Risks Related to Commercialization of Our Products

| |

• |

|

The commercial success of our planned or future products is not guaranteed. |

| |

• |

|

We may implement a product recall or voluntary market withdrawal, which could significantly increase our costs, damage our reputation, and disrupt our business. |

| |

• |

|

If we do not manage product inventory effectively and efficiently, it could adversely affect profitability. |

| |

• |

|

If we do not continue to obtain favorable purchase terms with manufacturers, it could adversely affect our operating results. |

Risks Related to Government Regulation

| |

• |

|

The nature of our business subjects us to compliance with employment, environmental, health, transportation, safety, and other governmental regulations. |

| |

• |

|

Product quality, warranty claims or safety concerns could impact our sales and expose us to litigation. |

Risks Related to Intellectual Property Matters

| |

• |

|

If we are unable to adequately protect our intellectual property rights, our competitive position could be harmed or we could be required to incur significant expenses to enforce or defend our rights. |

| |

• |

|

If we infringe on or misappropriate the proprietary rights of others, we may be liable for damages. |

Risks Related to Our Indebtedness

| |

• |

|

Our substantial indebtedness could materially adversely affect our financial condition and our ability to operate our business. |

| |

• |

|

Our ability to generate sufficient cash depends on numerous factors beyond our control, and we may be unable to generate sufficient cash flow to service our debt obligations. |

| |

• |

|

Restrictive covenants in the agreements governing our Credit Facilities may restrict our ability to pursue our business strategies, and failure to comply with these restrictions could result in acceleration of our debt. |

| |

• |

|

Incurrence of substantially more debt could further exacerbate the risks associated with our substantial leverage. |

| |

• |

|

The phaseout of the London Interbank Offered Rate (LIBOR), or the replacement of LIBOR with a different reference rate, may adversely affect interest rate. |

Risks Related to Ownership of Our Common Stock

| |

• |

|

Our stock price may be volatile, resulting in substantial losses for investors. |

| |

• |

|

Future sales of shares by existing stockholders could cause our stock price to decline. |

| |

• |

|

Stockholders’ ability to influence corporate matters may be limited because a small number of stockholders beneficially own a substantial amount of our common stock and continue to have substantial control over us. |

| |

• |

|

Transactions engaged in by our principal stockholders, our officers or directors involving our common stock may have an adverse effect on the price of our stock. |

| |

• |

|

We do not intend to pay dividends for the foreseeable future. |

| |

• |

|

Anti-takeover provisions in our charter and under Delaware law could limit certain stockholder actions. |

| |

• |

|

Certain provisions of our fifth amended and restated certificate of incorporation may have the effect of discouraging lawsuits against our directors and officers. |

| |

• |

|

We will continue to incur increased costs as a result of being a public company. |

| |

• |

|

If we are unable to effectively implement or maintain a system of internal control over financial reporting, we may not be able to accurately or timely report our financial results. |

| |

• |

|

We were previously a “controlled company” within the meaning of the corporate governance standards of Nasdaq, and, as a result, you may not have the same protections afforded to stockholders of other companies during the transition period afforded to us by the rules of Nasdaq. |

Our Corporate Information

We were incorporated as a Delaware corporation on February 6, 2007.

Our principal executive offices are located at 2005 East Indian School Road, Phoenix, Arizona 85016 and our telephone number is (602)

366-3999.

We maintain a website at the address www.lesliespool.com.

Information contained on, or accessible through, our website is not a part of this prospectus or the registration statement of which this prospectus forms a part, and you should not rely on that information when making a decision to invest in our common stock.

|

|

|

| |

|

Leslie’s, Inc. |

|

|

Common stock offered by the selling stockholders |

|

29,000,000 shares (or 33,350,000 shares if the underwriters exercise in full their option to purchase additional shares). |

|

|

Option to purchase additional shares |

|

The selling stockholders have granted the underwriters a 30-day option to purchase up to 4,350,000 additional shares of our common stock from the selling stockholders at the public offering price. |

|

|

Common stock to be outstanding immediately after the offering |

|

|

|

|

| |

|

The selling stockholders will receive all net proceeds from the sale of the shares of common stock to be sold in this offering, and we will not receive any of these proceeds. See the sections entitled “Use of Proceeds,” “Principal and Selling Stockholders” and “Underwriting.” |

|

|

| |

|

“LESL” |

Unless otherwise indicated, this prospectus reflects and assumes the following:

| |

• |

|

no vesting of the restricted stock units described below; and |

| |

• |

|

no exercise by the underwriters of their option to purchase additional shares of common stock. |

The number of shares of our common stock to be outstanding after this offering is based on 186,873,341 shares of common stock outstanding as of February 7, 2021, and excludes:

| |

• |

|

8,146,795 shares of common stock reserved for future issuance under our 2020 Omnibus Incentive Plan; |

| |

• |

|

5,690,649 shares of common stock issuable upon the settlement of restricted stock units outstanding as of February 7, 2021; and |

| |

• |

|

4,589,412 shares of common stock issuable upon the exercise of stock options outstanding as of February 7, 2021 under our 2020 Omnibus Incentive Plan, at a weighted average exercise price of $17.03 per share. |

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL AND OTHER INFORMATION

The following table sets forth our summary consolidated statements of operations data for the three months ended January 2, 2021 and December 28, 2019 and the years ended October 3, 2020, September 28, 2019, and September 29, 2018, and our consolidated balance sheet data as of January 2, 2021, December 28, 2019, October 3, 2020, September 28, 2019, and September 29, 2018. We have derived the following consolidated statements of operations data for the years ended October 3, 2020, September 28, 2019, and September 29, 2018, and the balance sheet data as of October 3, 2020, September 28, 2019, and September 29, 2018 from our audited consolidated financial statements included elsewhere in this prospectus. We have derived the following statements of operations data for the three months ended January 2, 2021 and December 28, 2019 and balance sheet data as of January 2, 2021 and December 28, 2019 from our unaudited interim consolidated financial statements. The unaudited interim consolidated financial data, in management’s opinion, have been prepared on the same basis as the audited consolidated financial statements and the related notes included elsewhere in this prospectus, and include all adjustments, consisting only of normal recurring adjustments, that management considers necessary for a fair presentation of the information for the periods presented. Our historical results are not necessarily indicative of the results that may be expected for any future period. The following summary consolidated financial data should be read with the sections titled “Selected Historical Consolidated Financial and Other Information” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes included elsewhere in this prospectus.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

| |

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Statement of operations data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

$ |

145,006 |

|

|

$ |

122,978 |

|

|

$ |

1,112,229 |

|

|

$ |

928,203 |

|

|

$ |

892,600 |

|

Cost of merchandise and services sold |

|

|

93,291 |

|

|

|

81,900 |

|

|

|

651,516 |

|

|

|

548,463 |

|

|

|

535,464 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

51,715 |

|

|

|

41,078 |

|

|

|

460,713 |

|

|

|

379,740 |

|

|

|

357,136 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selling, general and administrative expenses |

|

|

77,489 |

|

|

|

59,721 |

|

|

|

314,338 |

|

|

|

258,152 |

|

|

|

241,669 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

(25,774 |

) |

|

|

(18,643 |

) |

|

|

146,375 |

|

|

|

121,588 |

|

|

|

115,467 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

11,516 |

|

|

|

22,417 |

|

|

|

84,098 |

|

|

|

98,578 |

|

|

|

91,656 |

|

Loss on debt extinguishment |

|

|

7,281 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

| |

|

|

— |

|

|

|

137 |

|

|

|

1,089 |

|

|

|

7,453 |

|

|

|

1,759 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

18,797 |

|

|

|

22,554 |

|

|

|

85,187 |

|

|

|

106,031 |

|

|

|

93,415 |

|

Income (loss) before taxes |

|

|

(44,571 |

) |

|

|

(41,197 |

) |

|

|

61,188 |

|

|

|

15,557 |

|

|

|

22,052 |

|

Income tax benefit (expense) |

|

|

(14,314 |

) |

|

|

(15,010 |

) |

|

|

2,627 |

|

|

|

14,855 |

|

|

|

4,926 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

$ |

(30,257 |

) |

|

$ |

(26,187 |

) |

|

$ |

58,561 |

|

|

$ |

702 |

|

|

$ |

17,126 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

104,077 |

|

|

$ |

1,938 |

|

|

$ |

157,072 |

|

|

$ |

90,899 |

|

|

$ |

77,569 |

|

| |

|

|

355,627 |

|

|

|

242,926 |

|

|

|

372,133 |

|

|

|

282,089 |

|

|

|

255,332 |

|

| |

|

|

747,108 |

|

|

|

651,286 |

|

|

|

746,438 |

|

|

|